VAT in the Digital Age: How will Maltese Businesses be impacted?

All businesses selling goods or services within the European Union (EU), whether established in the EU or otherwise, will be impacted by the changes that the VAT in the Digital Age (ViDA) package adopted by the Council of the European Union (EC) adopted on 11th March 2025.

ViDA is a major EU initiative aimed at modernizing VAT regulations and reducing VAT fraud by simplifying compliance through digital reporting and e-invoicing. The reform that the ViDA package will bring along shall be implemented by all Member States by 2035.

What is Vat in the Digital Age (ViDA)?

The VAT in the Digital Age (ViDA) package is a major reform of the EU’s VAT system aimed at modernising VAT reporting across Member States. As technology advances and cross border transactions are on the rise, the Council of the European Union felt the need for the VAT system to evolve to reflect the new realities and simplify compliance across different member states and enhance the efficiency in the collection of VAT across the EU. The aim of ViDA is to narrow the gaps and inconsistencies within the current VAT system which leads to fraud, ambiguities and increase compliance burdens on businesses operating across multiple jurisdictions.

The ViDA initiative reflects the growing shift towards a digital and cross-border economy and seeks to address inefficiencies and fraud within the current VAT framework.

The ViDA packages is built around three pillars:

- Digital Reporting Requirements and e-invoicing

- The platform economy

- A Single VAT Registration system across the EU

These changes are intended to simplify compliance, reduce administrative burdens, and improve transparency in intra-EU transactions.

Pillar I: EU VAT Digital Reporting Requirements and E-invoicing

One of the most transformative aspects of ViDA is the introduction of Digital Reporting Requirements (DRR) and e-invoicing. Through the EU VAT digital reporting measure, the EU seeks to be in a position of identify missing trader intra-community VAT fraud and close the VAT gap in the shortest time possible.

Under this system, businesses will be required to:

- Issue structured electronic invoices (e-invoices) for intra-community B2B transactions

- Report transaction data in near real-time to tax authorities. The ViDA package provides that the deadline for issuing invoices for intra-community supplies or for which the reverse charge mechanism applies shall be of ten working days after the chargeable event takes place. Summary invoices for sales made within the same calendar month will still be allowed and should be issued within 10 days after the end of the calendar month.

Suppliers are required to report invoice data in real time i.e. at the time the invoice is issued or should have been issued. In cases of self-billing or reporting by the buyer, the buyer must transmit the information by not later than 5 days after the invoice is or should have been issued.

- Ensure invoices comply with the new digital reporting requirement system for intra-community transactions which will provide information on a transaction-by-transaction basis. The information collected from invoices will be uploaded on the risk analysis system of the Member States to help them combat VAT fraud. If the information is not transmitted in a timely manner or does not contain the correct information, the exemption with credit or 0 rated VAT for intra-community supplies would not be applied.

Traditional formats of invoices such as PDFs will no longer suffice unless structured data is embedded.

The objective is to enable tax authorities to access transaction-level data almost instantly, significantly reducing VAT fraud particularly in cross-border trade and improving data accuracy across Member States.

Pillar II: The platform economy

The second pillar under ViDA; the platform economy, introduces the ‘’deemed supplier’’ for VAT purposes for certain platforms operating in the short-term accommodation and passenger transport sectors. To this effect, as from 1 July 2028, digital platforms facilitating short-term accommodation rentals (up to 30 consecutive nights) or passenger transport by road within the EU will be treated as deemed suppliers meaning they will be treated as having received and re-supplied such services themselves and thus will be required to collect and remit VAT if the underlying providers do not collect and remit VAT themselves.

An exception to this treatment applies when the underlying provider supplies the platform with its own VAT identification number or if the underlying provider uses the new 2025 SME VAT registration special scheme for small enterprises.

With regards to the platform economy, it has been clarified that travel agents will not be considered as deemed suppliers and platform supplies are excluded from the Travel Operators Margin Scheme (TOMS).

Pillar III: Single VAT registration

The single VAT registration pillar under ViDA comes into effect as from 1 July 2028. This initiative is designed to reduce significantly the number of VAT registrations of a business across the EU. Under this initiative, businesses will be allowed to register for VAT in one member state; usually in the state where they are established, and address their VAT obligations in other member states via a single portal, hence reducing administrative burdens particularly for businesses engaged in cross-border supplies of goods across the EU.

In order to achieve the single VAT registration, the One-Stop-Shop (OSS) system will be extended to cover domestic supplies of goods, supplies with installation and assembly, supplies on board EU passenger transport and supplies of electricity, gas, heating and cooling.

The mandatory reverse charge rule will also be extended and will apply to all B2B supplies of goods and services where the supplier is not established and registered for VAT in the EU member state where VAT is due and the recipient of the good or service is identified for VAT purposes in that Member State. The supplier is still required to declare such supplies in his recapitulative statement and the supplies will fall within the scope of digital reporting obligations.

With respect to the transfer of own goods from one member state to another, a special scheme will be introduced to avoid the requirement of a person to be registered for VAT in the country of departure and country of arrival of goods. These transactions shall not be reportable in the company’s recapitulative statement. It is imperative to note that the special scheme for the transfer of own goods shall not be applicable in relation to goods where the person does not have full right of VAT recovery. In view of the new scheme to be implemented, the call-off arrangement will be abolished by 30th June 2028 and the ownership of goods must be transferred to the intended customer by 30 June 2029.

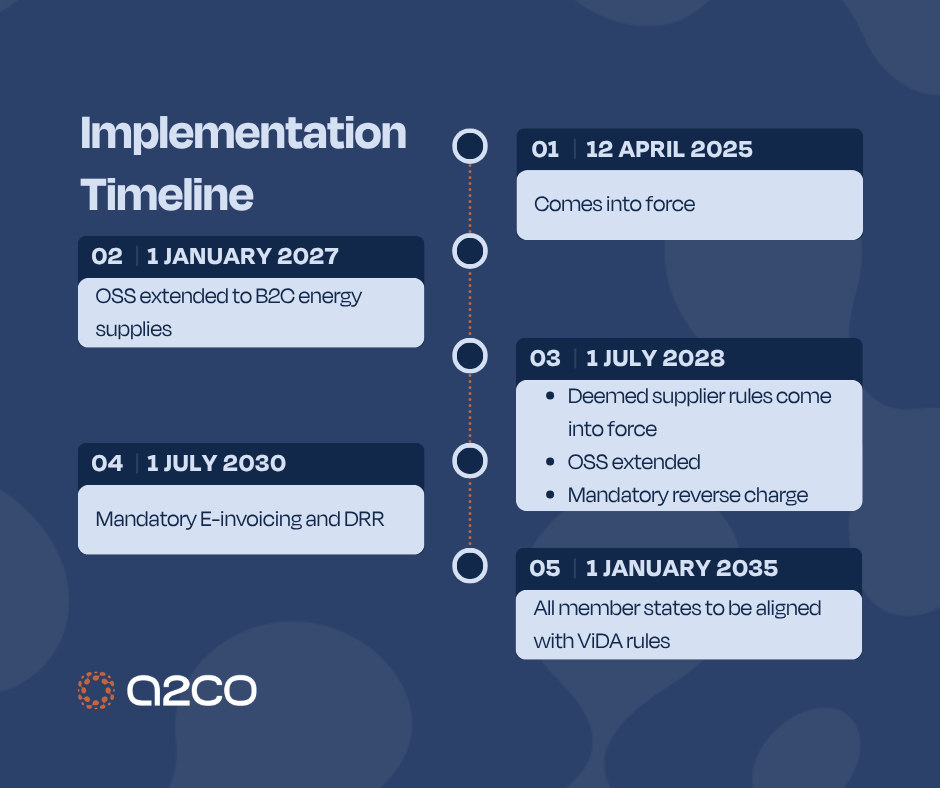

Implementation Timeline and VAT Reporting

The ViDA reforms will be introduced gradually, giving businesses time to adapt:

- 12 April 2025 – the ViDA package comes into force. Domestic e-invoicing is permitted without EU derogation. EC to adopt anti-fraud rules under IOSS.

- 1 January 2027 – OSS extended to B2C energy supplies.

- 1 July 2028 – Deemed supplier rules for platforms comes into effect; OSS extended to transfer of own goods and goods with installation; Mandatory reverse charge for certain B2B transactions

- 1 July 2030: E-invoicing and digital reporting for intra-EU B2B transactions becomes mandatory

- 1 January 2035: Deadline for Member States with existing national reporting systems to align with the EU-wide rules

Who Will Be Most Affected by ViDA?

While ViDA applies broadly to all businesses trading within the EU, certain businesses will be impacted more acutely than others. ViDA is especially relevant to:

1. Cross-border businesses

Companies supplying goods or services across EU Member States will face the most immediate changes due to mandatory e-invoicing and real-time reporting.

2. SMEs engaged in intra-EU trade

Smaller businesses may face disproportionate compliance costs due to system upgrades and process changes, despite simplification efforts.

3. Digital platforms

Platforms facilitating short-term accommodation or transport services will be subject to deemed supplier rules, shifting VAT obligations onto the platform itself.

4. Non-EU businesses trading into the EU

ViDA applies regardless of the country of establishment of the business. This means that non-EU entities selling into the EU will also need to comply with the new reporting standards.

Practical Steps Businesses Should Take to Be Compliant

The measures being implemented through the coming into force of the ViDA package is expected to revamp the VAT impact and compliance obligations of business operating cross-border. Since this change is expected to be significant, businesses should begin preparing well in advance for these changes. Key actions include:

1. Assess current VAT processes

Conduct a gap analysis to identify where existing invoicing and reporting systems fall short of ViDA requirements.

2. Upgrade IT systems

Invest in software capable of:

- Generating structured e-invoices

- Supporting real-time data transmission

- Integrating with ERP and accounting platforms

3. Review cross-border transaction flows

Map out intra-EU supplies to understand where DRR obligations will arise.

4. Train finance and tax teams

Ensure internal teams understand the operational and technical requirements of e-invoicing and reporting.

5. Monitor national implementation

Although ViDA is an EU initiative, its implementation may vary from member state to member state.

Implications for Malta-Based and Cross-Border Structures

Malta, as an EU Member State with a strong international business sector, is particularly exposed to the implications of ViDA.

For Malta-based companies:

- Increased compliance obligations for businesses engaged in intra-EU trade

- Potential need to overhaul existing accounting and invoicing systems

- Greater scrutiny from tax authorities due to real-time reporting

For cross-border structures:

- Reduced need for multiple VAT registrations through expanded OSS schemes

- Simplification of reporting for pan-European operations

- Increased transparency, potentially impacting tax planning structures

The shift to real-time reporting may also reduce the flexibility historically associated with VAT planning, requiring more robust and transparent structures.

Conclusion: A Defining Shift for Malta’s VAT Landscape

ViDA represents one of the most significant transformations of the EU VAT system in decades. For Malta, the reform is both a challenge and an opportunity.

On one hand, businesses will need to invest in systems, processes, and expertise to meet the new requirements. On the other, the harmonisation of VAT rules and reduction in administrative burdens; particularly through the Single VAT Registration, may enhance Malta’s attractiveness as a hub for international business.

Ultimately, early preparation will be critical. Maltese businesses that proactively adapt to ViDA will not only ensure compliance but also position themselves competitively in an increasingly digital and transparent EU tax environment.