MiCA Utility Token Issuance: What Founders Need to Know Before Launching a Utility Token in the EU

Why Utility Token Issuers Are Reassessing Launch Plans Under MiCA

Before the implementation of MiCA, token launches within the EU operated in a grey area. In many cases, speed mattered more than structure, and regulatory considerations were treated as a secondary consideration, if ever considered.

That environment has changed, particularly for founders planning or preparing to distribute tokens to EU users.

MiCA is now in force across the EU, and for token issuers this represents a clear shift in expectations. Token issuance is no longer viewed as informal or experimental from a regulatory perspective. Decisions taken at the design and launch stage now carry real consequences, particularly around how a token is classified and how it is presented to users.

This matters because early choices are difficult to unwind. The way a token is described, how it is distributed, and what rights or access it provides can all shape how regulators assess it later.

For founders planning a utility token or a token generation event, MiCA introduces a simple reality. You need clarity on your regulatory position before you go live, not after.

What MiCA Regulates When You Issue a Utility Token

One of the most common sources of confusion is scope. Many teams assume MiCA only applies to exchanges or custody providers. Others believe it only targets tokens which are backed by an asset or FIAT. While these cases remain subject to regulatory compliance, it is incorrect to assume that the token offered is entirely unregulated by any national competent authority.

Any intention to offer or make a utility token available to the public in the EU requires the issuer to undertake the applicable notification procedure under MiCA.

At the same time, MiCA does not regulate everything. Truly unique NFTs may fall outside scope. Certain closed loop instruments and limited use cases may also be exempt.

The real risk lies in assuming that an exemption applies without properly testing that assumption. Many founders do this unintentionally, relying on outdated market norms or informal advice that no longer reflects how regulation is applied under MiCA.

Utility Tokens Under MiCA and Why Classification Matters

MiCA does not rely on labels. Calling a token a utility token does not determine how it will be classified. Regulators focus on how the token works in practice and how it is presented to users, not on how it is described in marketing materials or internal documents.

When authorities assess a utility token under MiCA, they tend to focus on a small number of core questions. What access does the token actually provide. Is that access available at the time of issuance or only promised later. Can the token be transferred or traded. Is there an expectation of value, liquidity, or appreciation, even implicitly.

Problems arise when utility claims and economic reality do not align. Common patterns include tokens sold long before a product exists, access rights that are vague or discretionary, promotional language that emphasises value rather than use, or design choices that make secondary trading likely even if it is not the stated intent.

In these situations, founders often believe they are issuing a straightforward utility token. Regulators may see something very different.

Misclassification rarely comes from bad intent. More often, it comes from copying market practices that existed before MiCA came into force. Under the new regime, those shortcuts carry far greater risk.

MiCA White Paper Requirements for Utility Token Issuers

The white paper is often the first concrete concern founders raise. Even the idea of producing one can feel heavy or overly legalistic, particularly for early stage teams.

Under MiCA, a white paper is required when a token is offered to the public or admitting to trading in the EU, unless a narrow exemption applies. For many utility token projects, a white paper will be expected as part of the issuance process.

The purpose of the white paper is not marketing. It is disclosure.

Regulators use it to understand what the token does and does not do, how it is issued and distributed, what risks users face, and how the project is governed. In that sense, it functions as a reference point rather than a sales document.

In practice, many white papers fail not because they are too short or incomplete, but because they are unclear and do not follow the standard which is detailed in MiCA. Common weaknesses include blurring technical vision with actual functionality, avoiding clear statements about limitations, downplaying risks instead of explaining them, or creating inconsistencies between documentation and product design.

A strong MiCA white paper allows a regulator to understand the project without making assumptions. If it raises more questions than it answers, it quickly becomes a liability rather than a safeguard.

Governance Expectations for MiCA Utility Token Issuers

Some founders assume governance only becomes relevant once a project starts providing regulated services. That is not how MiCA is applied in practice.

Even at the issuance stage, regulators expect to see basic governance clarity. This does not mean complex board structures or heavy frameworks. It means being able to answer straightforward questions about how decisions are made and who ultimately controls the token.

Who decides on changes to the token. Who controls supply and issuance mechanics. How conflicts of interest are managed. What safeguards exist to protect users from obvious harm.

Common blind spots include founders retaining unchecked control without clear disclosure, assuming decentralisation without evidence, or failing to define accountability for token related decisions.

MiCA encourages projects to be honest about where control sits today, not where it might sit in the future. That honesty often matters more than ambition.

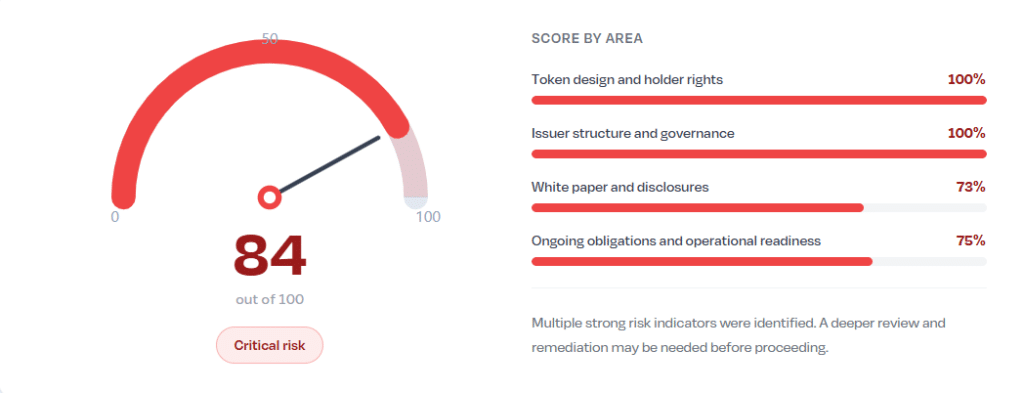

Assess Your Token Issuance Risk Before You Launch

Most teams do not need legal advice on day one. What they need first is clarity.

The Token Issuer MiCA Risk Index is designed as a practical diagnostic tool. It evaluates key risk areas that regulators typically focus on when assessing token issuance under MiCA.

This includes token functionality and access, distribution and transferability, disclosure readiness, and governance signals. The outcome is a structured risk score that highlights where a project is exposed, what requires attention, and what can reasonably wait.

The aim is simply to replace uncertainty with structure and give founders a clearer starting point.

Check your token issuance risk in minutes.

How We Support Token Issuers Navigating MiCA

Our role is not to sell templates or quote regulation. It is to help founders interpret MiCA as it applies to their specific token and launch strategy.

We support token issuers by challenging classification assumptions early, structuring disclosures so they make sense to regulators, and aligning token design choices with regulatory expectations. Where relevant, we bring insight from working with EU supervisory authorities, including in Malta, to help projects avoid friction later.

If a project evolves beyond issuance into regulated activity, we can support those next stages too. This page, however, is focused on helping you start on solid ground.